Updates on ESRS (European Sustainability Reporting Standards)

Introduction

This blog aims to provide an overview of the recent updates to ESRS (European Sustainability Reporting Standards) in June 2023. It is intended to inform the audience briefly of the relationship between Corporate Sustainability Reporting Directive (CSRD) (1) and ESRS, offer a clear understanding of the changes made in June 2023 to the ESRS Draft, and shed light on the implications it holds for businesses.

In this blog, we will be answering the following questions:

- What is ESRS?

- What does it mandate?

- How is ESRS relevant to CSRD and the updates?

- What changes or updates have been made?

- What are the next steps?

- What comes next for companies?

What is ESRS?

ESRS serves as a mandatory framework for sustainability reporting and is legally binding. Developed by EFRAG (2) (European Financial Reporting Advisory Group), ESRS enables corporations to disclose their sustainability performance in accordance with the CSRD, covering social and environmental risks and the impact of their activities on people and the planet. ESRS applies to all companies falling under the scope of CSRD and tailored for small and medium-sized enterprises (SMEs) and non-EU companies. Starting from the financial year 2024, which begins on or after January 1st, 2024, companies within the CSRD scope must adhere to ESRS for reporting purposes, with their reports due in 2025. A one-page infographic of the 7 key points of the CSRD is available here (3).

What does it mandate?

ESRS offers clear guidelines for sustainability reporting, outlining the required topics and indicators that companies must follow. These topics encompass critical areas such as climate change, diversity, biodiversity, human rights, labor practices, water and resource management, and anti-corruption measures. ESRS introduces the concept of double materiality (4), expanding the reporting scope to encompass the entire value chain of companies. This framework has a substantial influence on the breadth, volume, and level of detail required for disclosing information.

How is ESRS relevant to CSRD and the updates?

The Corporate Sustainability Reporting Directive (CSRD) ushers in a new era of sustainability reporting in the EU, requiring companies to disclose various environmental, social, and governance aspects. The ESRS (European Sustainability Reporting Standards) specify the detailed reporting requirements outlined by the CSRD.

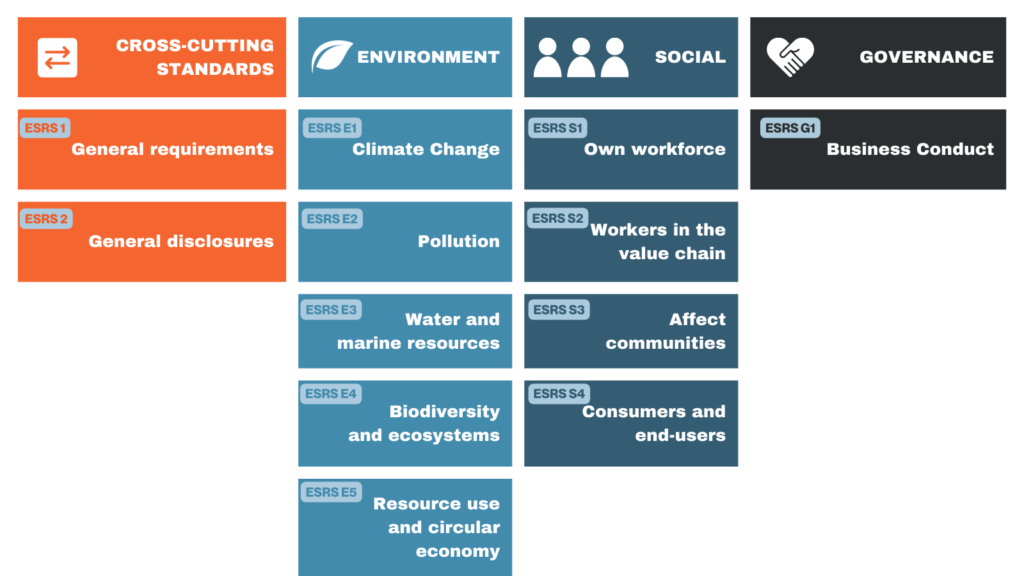

The 12 draft ESRS (5) include the following:

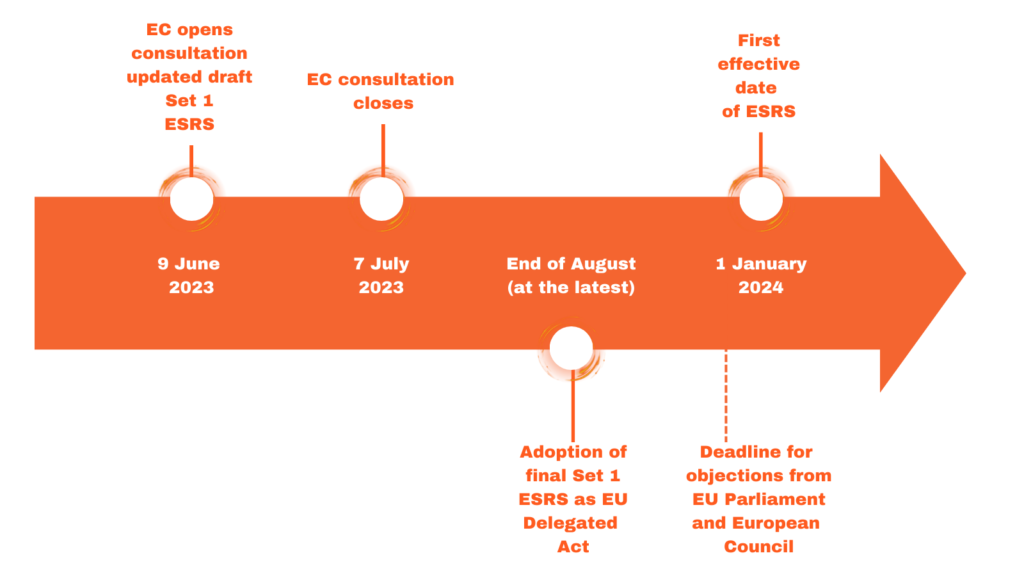

The legislative package (6) published June 2023, open for feedback until July 7th, 2023, consists of a draft delegated act that will make the ESRS legally binding in the EU. Appendix I of the document contains the revised draft ESRS, and Appendix II, includes a list of acronyms and a glossary of terms. This ESRS draft includes two specific standards regarding to all sustainability matters, and ten specific standards covering a broad spectrum of environmental, social, and governance topics.

What changes or updates have been made?

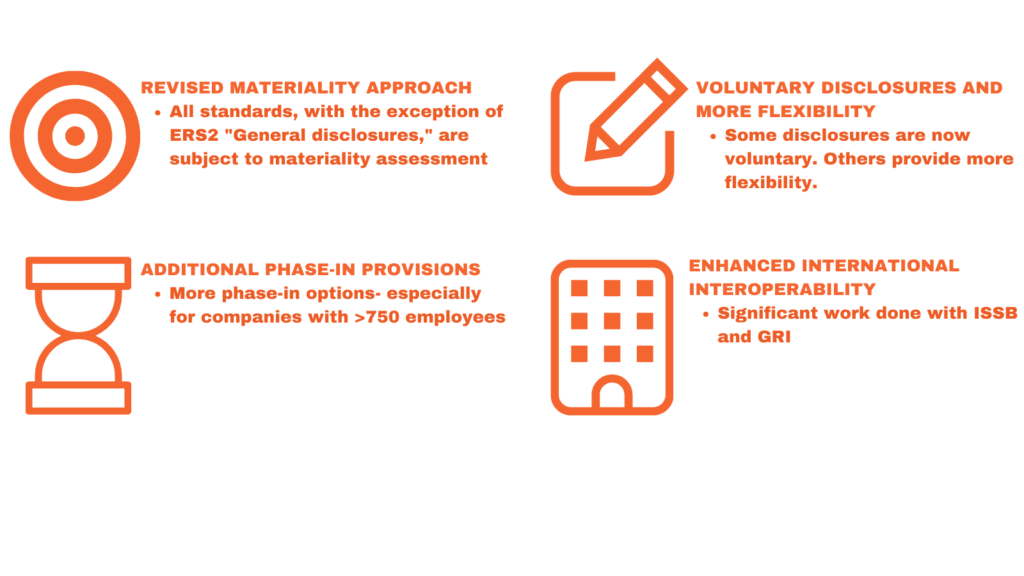

The European Commission has evaluated the draft ESRS from EFRAG to ensure compliance with the CSRD and alignment with the EU’s policy objectives under the European Green Deal. No changes were made to the overall structure. Nonetheless, the European Commission implemented modifications in four main areas to ease the reporting burden and facilitate the initial implementation of the standards.

Updates to ESRS:

- Materiality assessment: Except for ESRS 2 “General disclosures,” all standards require a materiality assessment. Companies need to determine which information is considered material based on this assessment. Previously, EFRAG drafts had mandatory disclosures. Now, if not material, these disclosures are no longer required. Only the “General disclosures” in ESRS 2 will be mandatory.

- Voluntary disclosures: Certain disclosures are now optional. For instance, companies can choose whether to disclose the transition plan for biodiversity and ecosystems (ESRS E4), as well as information about non-employee workers in ESRS S1, such as wages, social protection, and health and safety. Additionally, explaining why certain sustainability topics are deemed not material is also a voluntary disclosure.

- Additional phase-in provisions: The European Commission has introduced phase-in provisions and simplified reporting requirements for anticipated financial effects on companies involved. Here’s a summary:

- In the first reporting year, companies can exclude reporting on financial effects from climate and environmental impacts, risks, and opportunities.

- For the first three years of reporting, companies can provide qualitative disclosures for financial effects, with some exceptions. If it’s impractical, quantitative disclosures for climate-related financial effects can be omitted.

- Certain disclosure requirements related to the company’s own workforce, such as social protection, employees with disabilities, health and safety, and work-life balance, may be omitted in the first reporting year.

- Companies with less than 750 employees have special relief:

- In the first reporting year, they can omit all workforce-related disclosures and greenhouse gas emissions related to climate change.

- In the first two reporting years, they can omit reporting on biodiversity, ecosystems, workers in the value chain, affected communities, and consumers and end-users.

- Interoperability: The European Commission has collaborated closely with the International Sustainability Standards Board (ISSB) and the Global Reporting Initiative (GRI) to ensure that ESRS aligns with global standard-setting initiatives. The draft ESRS has been modified based on this collaboration. After the release of the final ISSB standards on 26th June 2023, a comprehensive analysis will be conducted to assess the extent to which reporting duplication can be minimized and ensure compatibility.

What are the next steps?

The feedback period for the “near final” ESRS ends on July 7, 2023. Companies can provide their responses through the feedback template on the European Commission’s website. The final ESRS version will become EU law through a delegated act by the European Commission. To ensure ESRS applies to financial years starting on or after January 1st, 2024, adoption must occur before the end of August 2023. After adoption, there will be a two-month scrutiny period by the European Parliament and Council, which could be extended to four months. If no objections are raised, ESRS will come into effect on January 1st, 2024. However, if objections are raised, the standards cannot be modified, and the process for the first set of ESRS would need to restart.

What comes next for companies?

After the latest updates to ESRS, companies under CSRD must prepare for new reporting requirements, regardless of their sustainability maturity.

Conducting an impact assessment and double materiality analysis is crucial to identify relevant ESG factors. A gap analysis evaluates existing data alignment with ESRS and other frameworks. Defining sustainability disclosure ambition, considering ISSB, CDP, Ecovadis, etc., and identifying appropriate data sources are essential steps.

Meeting CSRD and ESRS involves considering IT system impact, expanding reporting processes with change management, fostering a sustainable culture, and aligning teams with sustainability goals. Employee training and collaboration with stakeholders enhance transparency in the supply chain.

The path forward requires a comprehensive and strategic approach, involving commitment from all levels of the organization. Proactive steps to improve data collection and reporting processes position companies as responsible corporate citizens, positively impacting society and the environment.

Reference:

(1) For more details, refer to

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32022L2464&from=FR, Official Journal of the European Union, 2022

(2) European Financial Reporting Advisory Group, https://www.efrag.org

(3) Infographic “The 7 key points of the CSRD”, https://www.kshuttle.io/en/csrd-infographic/, kShuttle website, 2023.

(4) Double Materiality, https://www.kshuttle.io/en/article-towards-double-materiality-inputs-from-efrags-work-for-the-csrd/, kShuttle website, 2023

(5) Draft ESRS, https://efrag.org/lab6

(6) Legislative Package, https://ec.europa.eu/info/law/better-regulation/have-your-say/initiatives/13765-European-sustainability-reporting-standards-first-set_en

To go further

https://nordesg.de/en/revised-version-of-the-european-sustainability-reporting-standard-esrs/

https://www.greenbiz.com/article/csrd-csddd-esrs-and-more-cheat-sheet-eu-sustainability-regulations