ESG reporting: the final version of the ESRS datapoints is finally out!

Friday night (31/05/2024), the EFRAG published the final version of its Implementation Guidance on ESRS datapoints, the famous “data points” that correspond to the information to be communicated in the ESG reporting of companies subject to CSRD.

Reminder of the context

At the end of December 2023, the EFRAG published their first three draft Implementation Guidance documents on the implementation of the ESRS and solicited a public consultation until February 2, 2024. The EFRAG received and reviewed 46 responses to the online survey from respondents. The discussions that followed during the EFRAG TEG (Technical Expert Group) and SRB (Sustainability Reporting Board) meetings led to this final version of the list of the data points, known as “EFRAG IG 3 : List of ESRS Datapoints”. This document presents the complete list of all disclosure requirements in the sectoral standards in an Excel format. The Excel file covers all standards, except for the ESRS 1 General Requirements, which does not define specific information to be provided. The implementation guidance is intended to help companies prepare their first sustainability report in accordance with the ESRS.

What does the final version of the ESRS data points introduce and modify?

- Addition of hyperlinks

In a very pragmatic approach, EFRAG has added hyperlinks to its final version, allowing users of the Excel document to directly access the Disclosure Requirements (DR) or Application Requirements (AR) section related to the data point.

2. Identification of conditional and alternative data points

The new version of the data points include a note in a separate column to indicate whether it is a conditional or alternative data point.

- A data point is considered conditional when it is only required to be reported if a specific precondition is met. For instance, fuel consumption data for coal (E1-5_10), oil (E1-5_11), natural gas…, etc., should only be reported if the company consumes these types of fuels.

- An alternative data point allows for a company to choose one over another for reporting. Therefore, if a company decides to publish one of these metrics, it is not obligated to report the others as well. For instance, it is appropriate to report greenhouse gas emissions according to ISO 14064 (E1-6_04) OR according to the GHG Protocol (E1-6_05).

These concepts are distinct from the voluntary qualifier (“may”) that is specified in another column. In that case, the company may choose to report or not report a voluntary indicator.

ESRS conditional, alternative and voluntary datapoints of ESRS E1 – Climate change

3.Improvement of references to “phase-in” transitional provisions

The content of the phase-in provisions column has been revised to include the duration of the period. More specific references have also been provided regarding the applicability of the transitional provisions.

Data points with phase-in provisions of 1 or 3 years from ESRS E5 – Circular Economy

4. Addition of an “ID”

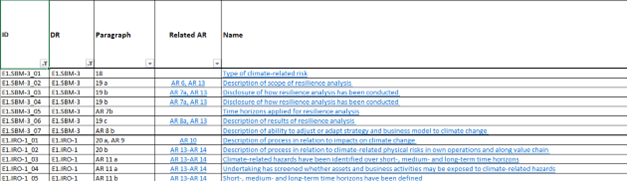

EFRAG has added an “ID” reference to each data point to allow them to be assigned a unique reference.

Unique references in the “ID” column on ESRS E1 – Climate change

5. Specific modifications

In response to feedback received, EFRAG has made changes to certain data points. These changes address the following:

- Added data points (6), deleted data points (36), merged data points (18). A comprehensive list of these modifications is available in the document Feedback statement – EFRAG IG: List of ESRS Data Points, starting on page 11.

- Modified data points

- Reclassification of data points as voluntary or mandatory

- Revision of references to the respective ESRS paragraphs (DR and AR)

6. Revision of instructions

Finally, this final version includes more specific instructions at the top of each sheet on data points to be reported regardless of the double materiality assessment. Additionally, there’s a reminder on disclosure information not only explicitly required by the ESRS, but also entity-specific information and information arising from other relevant legislation or standards.

Instructions at the top of the sheet dedicated to ESRS E4 – Biodiversity and ecosystems

Conclusions

EFRAG’s final version proposes substantial and very useful improvements for ESG reporting preparers. However, it is regrettable that EFRAG did not detail all the changes made to each data point: it is up to the users to compare with the previous version. It is also a shame about the timing: companies eligible from 2024 have already started preparing their first sustainability report and will have to redo a certain number of tasks. As it is just a few months away from the first reporting campaign, it would have been more useful to focus efforts elsewhere…

EFRAG documents available online :