The end all, be all on double materiality, based on EFRAG’s guidelines

The Corporate Sustainability Reporting Directive (CSRD) is set to take effect progressively from January 1st, 2024. As companies gear up for compliance, a central concern rises: what is “double materiality” and how are they meant to carry out their first “double materiality assessment.” Fear no more: the European Financial Reporting Advisory Group (EFRAG) has published a set of implementation guidelines for materiality assessment aimed at aiding companies in navigating the intricacies of materiality assessment.

CSRD / ESRS approach to materiality

The framework organizing sustainability reporting under the CSRD, now known as the European Sustainability Reporting Standards (ESRS), requires that companies’ sustainability statement include sustainability information related to material impacts, risks, and opportunities (IROs) identified through a materiality assessment process that applies the principle of double materiality.

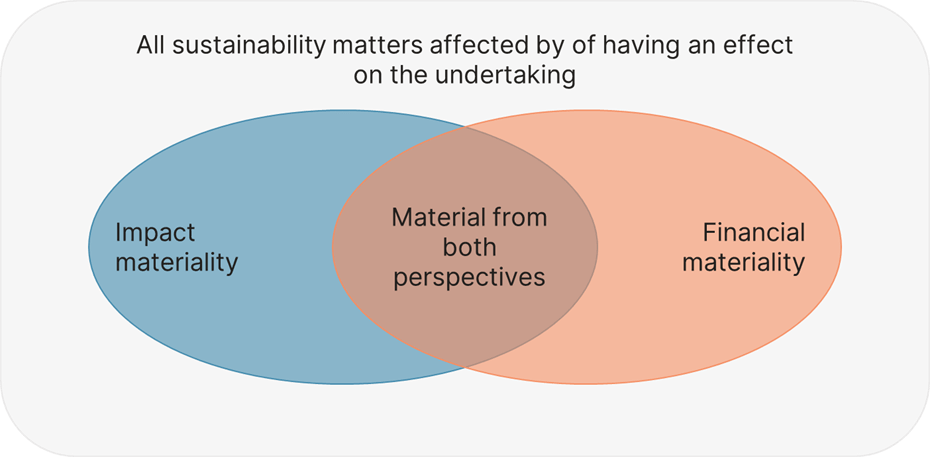

The concept of double materiality, originally introduced by the European regulation NFRD (Non-Financial Reporting Directive), encompasses both impact and financial perspectives, recognizing that materiality can arise from either or both dimensions.

ESRS 1 defines the two dimensions as follows: « A sustainability matter is material from:

- an impact perspective when it pertains to the undertaking’s material actual or potential, positive, or negative impacts on people or the environment over the short-, medium- and long-term. Impacts include those connected with the undertaking’s own operations and upstream and downstream value chain, including through its products and services, as well as through its business relationships” (ESRS 1 paragraph 43);

- a financial perspective if it triggers (or could reasonably be expected to) material financial effects on […] the undertaking’s development, financial position, financial performance, cash flows, access to finance or cost of capital over the short-, medium- or long-term” (ESRS 1 paragraph 49).The financial materiality assessment shall cover information that could reasonably be expected to influence decisions made by the primary users of general-purpose financial reports, including investors, regarding a company’s future.

Figure 1: impact and financial materiality, adapted from EFRAG’s guidance on double materiality

Benefits of the “double materiality” principle

The main benefits of this approach are as follows:

- Implementation of a standardized methodology, for greater efficiency and comparability;

- A formalized process for identifying ESG matters and material impacts, risks, and opportunities, engaging all stakeholders;

- An integrated approach which encompasses both financial and sustainability matters, fostering a company’s sustainable transition.

Juggling the key concepts

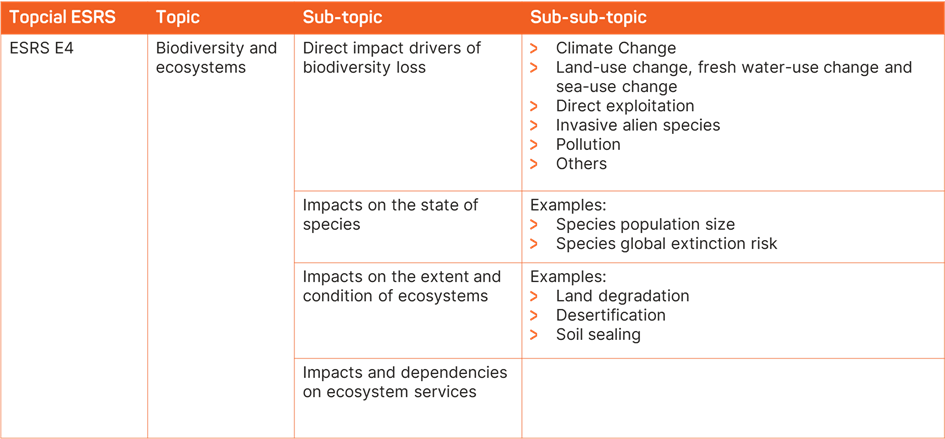

There are three categories of ESRS: cross-cutting standards; topical standards; and sector-specific standards (expected in 2025).

However, those of interest for the materiality assessment are the topical standards, as they cover the sustainability matters companies must report on:

- Environmental issues, aligned with the objectives of the European taxonomy: climate change (mitigation and adaptation); pollution; water and marine resources; biodiversity and ecosystems; resource use and circular economy.

- Social issues: own workers; workers in the value chain; affected communities; consumer and end-users.

- Governance issues: business conduct.

These matters are then divided into topics, sub-topics and sub-sub-topics.

Figure 2: ESRS E4 topic, sub-topics and sub-sub-topics (from ESRS 1 – Appendix A – AR 16)

The fundamentals of materiality assessment and sustainability reporting

- Goal: identify material impacts, risks, and opportunities (IROs) related to sustainability matters.

- How: assess materiality if material impact/financial effects arise from a matter.

- What: Once a matter has been identified as material, refer to the disclosure requirements in the respective topical ESRS to identify the information they must disclose. If a matter is not material, the company must state so. If the topic is material but not covered by ESRS, the undertaking shall disclose additional entity-specific disclosures.

Criteria for the identification of material information

To assess whether a matter is material, a company applies criteria based on relevance (ESRS 1 § 31):

- Significance of information in relation to the matter.

- Decision-usefulness for users.

General requirements for qualitative information also apply : relevance, faithful representation, comparability, verifiability, and understandability.

Materiality assessment: a step-by-step guide

ESRS do not prescribe a one-size-fits all materiality assessment process. Companies must design their own, ensuring it covers the full scope of ESG matters and reflects both impact and financial materiality, and interconnections between them.

EFRAG, in its guidance on how to implement the materiality assessment, introduces a process aligned with the ESRS which includes four steps companies may follow when conducting their materiality assessment.

Figure 3: The four-step approach of the materiality assessment)

Step 1. Know your business

> Develop an overview of activities, business relationships, and key stakeholders.

To do so, companies may need to:

- Analyze their business plan, strategy, financial statements, legal/regulatory landscape, and relevant published documents (media reports, sector-specific benchmarks, etc.).

- Map their activities, geographic locations, products and/or service generated, business relationships and upstream/downstream value chain.

- Understand which of their stakeholders are (likely to be) affected by their operations and/or their value chain, and what their views and interests are on sustainability matters.

Step 2. Identify the actual and potential IROs related to sustainability matters

> Create a “long list” of IROs relating to ESG matters across own operations / value chain.

Refer to ESRS 1 AR16, sector-specific standards and/or other reporting standards, such as the IFRS industry-based guidance, SASB Standards and GRI Sector Standards. Consider whether these IROs relate to own operations and/or value chain, and time horizon.

EFRAG identifies two ways to fulfill this step:

- Top-down approach: a company could start by identifying matters from the list provided in ESRS 1 AR 16 and then complete it by additional entity-specific matters, informed by existing reporting, internal processes, or stakeholder engagement. This approach should be favored by companies that are new to sustainability reporting.

- Bottom-up approach: a company may start by listing IROs based on its review of its business model, strategy, own operations, value chain and other research.

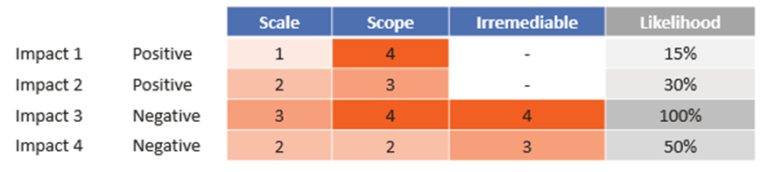

Step 3. Assess and determine the material IROs

a) Impact materiality assessment

Go through the list of IROs identified in Step 2 and use appropriate quantitative and/or qualitative thresholds to assess the materiality of current and potential impacts.

The following criteria must be applied:

- For actual impacts: scale, scope, and if the impact is negative, irremediable character of the impact.

- For potential impacts (positive or negative): likelihood of occurrence in relation with the severity of the impacts, and time horizon (short-, medium- or long-term).

Figure 4: Example of assessment of the impacts based on the criteria recommended by EFRAG

kShuttle recommends that companies define what the scales refer to as precisely as possible, and make the assessment as objective as possible to limit interpretation.

b) Financial materiality assessment

The following criteria must be applied:

Likelihood of occurrence

Potential magnitude of the financial effects

Time horizon (short-, medium- or long-term)

Information is considered financially material if omitting, misstating or obscuring it could reasonably be expected to influence (investment) decisions.

If measuring financial effects is not possible, kShuttle recommends identifying other types of risks that could have a financial impact on the company: operational risks, legal risks, or even reputational risks.

c) Consolidation

Consolidate the results from both assessments and consider the interactions (similarities and differences) between impact materiality and financial materiality.

Step 4. Report the material IROs in the sustainability statement

Incorporate material IROs into the sustainability statement, in the form of a double materiality matrix for example.

Stakeholder involvement

ESRS distinguishes between affected stakeholders and users of the sustainability statement. Affected stakeholders (internal and/or external) play a crucial role in the materiality assessment, providing input and feedback. If direct consultation is not feasible, alternatives like engaging credible independent experts (NGOs, scientific committees, etc.) should be explored.

In conclusion

ESRS distinguishes between affected stakeholders and users of the sustainability statement. Affected stakeholders (internal and/or external) play a crucial role in the materiality assessment, providing input and feedback. If direct consultation is not feasible, alternatives like engaging credible independent experts (NGOs, scientific committees, etc.) should be explored.