The SBTi has become a leading framework for setting credible climate targets. A closer look at its requirements, methodologies and implications for companies.

Faced with accelerating climate disruption and growing pressure from regulators, investors and stakeholders, companies are now expected to demonstrate their ability to manage a decarbonisation pathway that is credible, measurable and aligned with climate science.

In this context, the Science Based Targets initiative (SBTi) has emerged as the international reference framework for structuring robust and comparable climate targets.

But beyond climate science, what does an SBTi approach actually involve? What are the operational and strategic implications for companies? And what changes should organisations anticipate in the near term?

In practice, an SBTi approach consists of translating a global climate objective into a company-level decarbonisation pathway, based on a greenhouse gas inventory, a reference year, clearly defined emissions scopes and reduction targets monitored over time.

The SBTi: a standard born from the Paris Agreement

The SBTi was launched in 2015, in the wake of COP21, with a clear ambition: to translate global climate goals – limiting warming to 1.5°C or well below 2°C – into operational decarbonisation pathways for companies.

What makes the initiative distinctive is its alignment with the latest recommendations from climate scientists, in particular the work of the IPCC, the Intergovernmental Panel on Climate Change, established in 1988.

The carbon budget: the starting point for the pathway

At the heart of the SBTi approach lies the concept of a global carbon budget: the maximum amount of greenhouse gases that can still be emitted while staying below a given warming threshold – around 900 GtCO₂e to remain below 2°C by 2100.

Because this budget is limited, it needs to be allocated over time, broken down by sector and region, and translated into targets for individual companies. This is precisely where the value of the SBTi lies.

The framework fundamentally changes the nature of climate commitments. It is no longer enough to announce an ambition. Companies must demonstrate that their targets are compatible with a physical constraint: a finite volume of remaining emissions at global level.

The logic of the SBTi therefore rests on a simple principle: a company can no longer set a climate target based solely on its own internal ambition; it must demonstrate that this target is consistent with a pathway aligned with the scientific limits of global warming.

A response to the credibility gap in corporate climate commitments

Unlike traditional voluntary commitments, often criticised for lacking ambition or remaining purely declarative, the SBTi introduces several key principles:

- independent validation of targets;

- mandatory alignment with climate models;

- standardisation to enable comparability across sectors.

From voluntary framework to market quasi-standard

Adoption has accelerated rapidly. More than 10,000 companies have already had SBTi decarbonisation targets validated, representing over 40% of global market capitalisation.

France stands out in particular, with 85% of CAC 40 companies engaged and strong mobilisation among mid-sized companies and SMEs.

This rapid spread reflects a major shift: the SBTi is no longer simply a CSR tool. It has become a marker of financial and strategic credibility.

Companies identify several key benefits: stronger investor relations, easier access to financing, improved internal strategic alignment and greater engagement across the value chain.

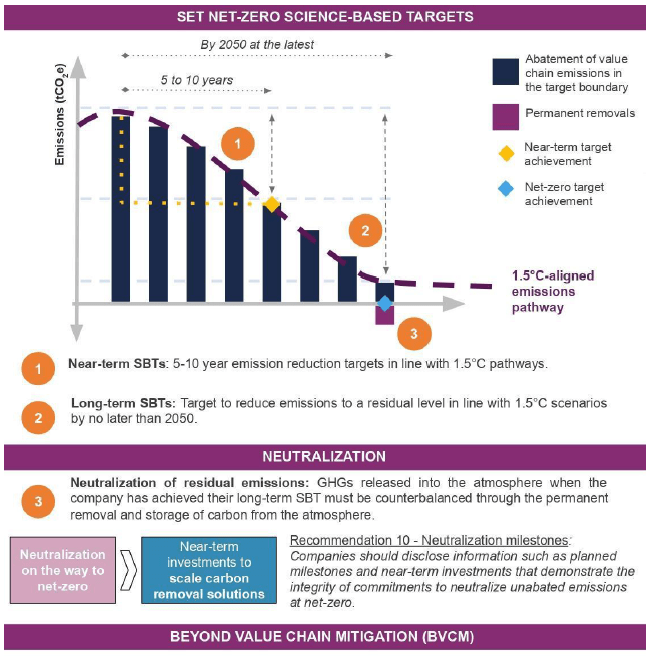

Reduce first, compensate later: the SBTi hierarchy

The SBTi is built on a simple but structuring principle: reduce first, compensate later – never the other way around.

A company aligned with the SBTi Net-Zero pathway must follow four broad stages:

- near-term emissions reduction over 5 to 10 years;

- long-term emissions reduction up to 2050;

- neutralisation of residual emissions, generally around 10%, only once emissions have been reduced by 90% to 95%;

- beyond value chain mitigation, known as BVCM.

Actions outside the value chain, now increasingly referred to as “contributions” rather than “offsets”, cannot replace internal emissions reductions, which remain the priority.

An SBTi process in four main phases

Companies seeking validation of their decarbonisation targets by the SBTi begin by making a public commitment to set a science-based target. They then have up to 24 months to develop that target.

The next stage is submission and validation – or non-validation – of the target, a process that can take around three to four months. Once the targets are validated, companies communicate them publicly.

The SBTi lists all companies engaged in the process in a publicly accessible database via its Target Dashboard.

How to build an SBTi target – A five-step methodology

Building an SBTi target is based on a rigorous process:

- choose a base year after 2015;

- calculate a complete greenhouse gas inventory using the GHG Protocol;

- define the relevant scopes;

- set a target year, typically 2030 and/or 2050;

- select the appropriate pathway methodology.

Scopes 1, 2 and 3: strong requirements on coverage

For Scopes 1 and 2, coverage must be almost exhaustive, at 95% or more. Scope 3 must be included in near-term targets if it represents more than 40% of total greenhouse gas emissions.

This is a structuring point, because for many companies, Scope 3 accounts for the largest share of their carbon footprint.

It should also be noted that additional criteria apply when setting long-term targets.

Three approaches to building an SBTi pathway

There are three main approaches to building an SBTi pathway.

The most common approach is based on the direct reduction of emissions in absolute terms, measured in tonnes of CO₂ equivalent. This is known as the Absolute Emissions Contraction approach. Its main advantage is that it can be easily aligned with IPCC scenarios.

A sector-based approach can also be used and is recommended as a priority by the SBTi where available. Because it relies on physical activity data, it is generally more precise and better suited to the specific decarbonisation challenges of a given sector. The most widely used methodology is the SDA, or Sectoral Decarbonisation Approach.

As a last resort, companies may also use an economic intensity approach, which calculates the required emissions reduction per unit of value added.

Net-Zero V2: a major evolution to anticipate

The SBTi’s flagship standard is currently undergoing a major transformation: the Corporate Net-Zero Standard V2 is expected by summer 2026.

That said, companies have no reason to wait before submitting their decarbonisation targets, as the current version of the standard can be used until the end of December 2027.

The main expected changes

The key challenge for this new version will be to introduce more flexibility while preserving the scientific rigour that lies at the heart of the SBTi.

Several new requirements have already been announced, including continuous monitoring of climate performance, mandatory progress assessment and the publication of a transition plan.

The concept of OER – Ongoing Emissions Responsibility – is also expected to be introduced, requiring companies to take continuous responsibility for their residual emissions rather than waiting until the 2050 horizon.

Carbon credits and related mechanisms are therefore expected to be more tightly framed, particularly to clarify their role in addressing residual emissions and supporting climate action beyond the value chain.

What this changes for CSR and finance teams

The SBTi requires quantified trajectories, interim milestones and annual reporting. This marks a shift from a declarative approach to a managed approach. In other words, the SBTi brings carbon management closer to financial performance management.

It is becoming embedded at the heart of corporate strategy, because its impacts are cross-functional: industrial strategy, procurement and supply chains, investment decisions and energy policy are all affected.

This also highlights the growing importance of data and information systems in managing the complexity of the requirements. Companies need robust data collection systems, traceability and the ability to simulate decarbonisation pathways over time.

The main operational challenge of an SBTi pathway therefore lies in the data itself: its quality, traceability, availability and ability to be managed year after year.

Conclusion: from climate framework to strategic standard

The Science Based Targets initiative marks a major turning point in the way companies approach climate action.

It transforms an environmental constraint into a structuring strategic framework and a tool for economic and financial credibility.

But this rise in importance also comes with challenges: methodological complexity, the need for reliable data, internal alignment and rapidly evolving standards.

For CSR, finance and reporting teams, the question is no longer whether to engage with the SBTi, but how to turn it into a lever for sustainable operational and strategic transformation.

In other words, the SBTi is not only about getting a target validated. It requires companies to organise their ability to manage decarbonisation over time.

Go further

While the definition of SBTi targets is based on strict scientific frameworks, their implementation depends above all on a company’s ability to structure, secure and manage its carbon data.

This is precisely where kShuttle supports its clients.

Q&A

The Science Based Targets initiative, or SBTi, is an international framework that enables companies to set greenhouse gas reduction targets aligned with climate science and the goals of the Paris Agreement.

It aims to turn climate commitments into measurable, comparable and validated decarbonisation pathways based on recognised criteria.

An SBTi pathway enables a company to demonstrate that its climate targets are based on a structured methodology and are compatible with the physical limits of global warming.

It strengthens the credibility of climate commitments, supports dialogue with investors and helps CSR, finance and reporting teams manage decarbonisation over time.

Scope 3 often represents the largest share of a company’s carbon footprint, as it covers indirect emissions across the value chain: purchasing, transport, product use, suppliers and end-of-life impacts.

Under SBTi criteria, Scope 3 must be included in near-term targets when it represents 40% or more of total Scope 1, 2 and 3 emissions. Near-term targets must also cover at least 95% of direct Scope 1 and 2 emissions.

The main challenges are not only methodological. They also relate to the company’s ability to produce reliable, traceable and regularly updated carbon data.

An SBTi approach requires organisations to structure their greenhouse gas inventory, improve the reliability of Scope 3 data, monitor progress over time and connect the climate pathway with operational and financial decision-making.

Not necessarily. The SBTi is currently revising its Corporate Net-Zero Standard Version 2.0, with a second public consultation published in 2026. The aim is to make the standard more robust and applicable for companies, while maintaining scientific integrity.

For companies, the priority is therefore to monitor the evolution of the framework without necessarily pausing the structuring of their climate pathway. The fundamentals remain the same: greenhouse gas inventory, credible targets, reliable data, governance and long-term management.