The European Commission's proposal for a Directive Omnibus: here's what to expect from your CSRD sustainability report!

Introduction

On February 26, 2025, the European Commission presented its proposal for a “simplification” Omnibus Directive.

This series of texts aims to lighten the administrative burden on European companies by amending 5 texts: the CSRD (sustainability reporting), the CS3D (duty of care), the taxonomy, the MACF and the InvestUE program.

In this article, we tell you more about the proposed revisions to the CSRD!

1. Initial objectives of the CSRD

Coming into force in January 2023, the Corporate Sustainability Reporting Directive (CSRD) is a major text of the European Green Deal and Sustainable Finance Action Plan. The CSRD aims to ensure that investors have the information they need to understand and manage the risks to which invested companies are exposed as a result of climate change and other sustainability issues.

Behind this text lies the aim of directing financial resources towards companies pursuing sustainable development objectives, and creating greater accountability and transparency towards all stakeholders with regard to ESG performance.

2. Political context: preserving and protecting the EU’s values, economy and competitiveness

War in Ukraine, rising energy prices, a changing and even “hostile” geopolitical landscape, differentiated approaches to sustainability reporting in other jurisdictions, etc.: the European Commission (EC) is using a changing geopolitical and economic context to review the requirements and content of sustainability reporting. The European Commission (EC) is relying on a changing geopolitical and economic context to review the requirements and content of sustainability reporting.

At the end of January, the European Commission announced its “Competitiveness Compass”, aiming to reduce costs by 25% for large companies and 35% for SMEs. The EC’s aim is to preserve and protect the EU’s values, its economy and its competitiveness.

3. Objectives of the European Commission’s revision of the CSRD

The proposed Omnibus Directive aims to clarify, simplify and streamline the requirements for sustainability reporting, in order to reduce the administrative and financial burden of reporting and its impact on small businesses. In particular, the EC points the finger at compliance costs and the zeal of auditors.

However, the Commission does not intend to “compromise the political objectives of these two pieces of legislation (i.e. CSRD and CSDD) and ensure a more cost-effective implementation of the overall ambition of the European green market linked to the green and fair transition”.

4. The content of the revisions proposed by the European Commission

Scope and timetable

To achieve its objectives of simplification and streamlining, the EC intends to revise the scope, implementation schedule and content of the sustainability report. Here are the details of these proposals.

Scope and timetable:

1. Reduce the number of companies required to publish a sustainability report by 80% and align the thresholds with the CSDD:

- Review of the scope of application by raising the threshold: this would apply to organizations employing more than 1,000 employees over the reporting period, with sales >50M€ or a balance sheet >25M€.

- This would have the effect of excluding companies with <1,000 employees, including wave 1, wave 2 and listed SMEs!

- As a result, the CSRD will now only concern 10,000 companies, compared with the initial 50,000.

2. Create a proportionate standard for voluntary use by companies not required to publish a sustainability report:

- This standard would be based on the ‘VSME’ standard developed by EFRAG, adopted in the form of a delegated act (with no need for transposition into national law).

- The EC intends to publish a recommendation on voluntary sustainability reporting based on EFRAG’s work.

3. Reduce trickle-down effects on SMEs by imposing the VSME standard as a value chain cap for all companies not required to publish a sustainability report.

4.defer publication by 2 years for so-called ‘wave 2’ companies (large unlisted companies) and ‘wave 3’ companies (listed SMEs) to avoid these companies publishing a report on FY2025 or FY2026 and then being exempted from the obligation to publish a report.

On concrete implementation

1. Lighten and simplify the content of cross-sector ESRS standards (known as “Set 1”):

- Reduce the number of mandatory indicators, clarify the distinction between mandatory and voluntary data, give priority to quantitative data over narrative information, simplify the structure and presentation of ESRSs, and ensure that companies disclose only meaningful and necessary information.

- Ensure alignment of ESRS standards with other regulations.

The EC wishes to publish the content of the new ESRS (i.e. adopt the ESRS delegated act) no later than 6 months after the entry into force of the proposed Omnibus Directive.

2. Eliminate the creation of sector-specific standards to avoid increasing the number of datapoints to be reported.

3. Cap the assurance level of the sustainability report at limited assurance:

- Remove the requirement for reasonable assurance. This is intended to limit audit costs.

EC to publish insurance guidelines by 2026

4. XBRL digital tagging is retained:

- The markup will be adopted by delegated act once the European Commission has received ESMA’s technical opinion.

- In terms of concrete implementation, EFRAG will have to redraft the nomenclature of the tags following the review of ESRS as proposed in the Omnibus Directive.

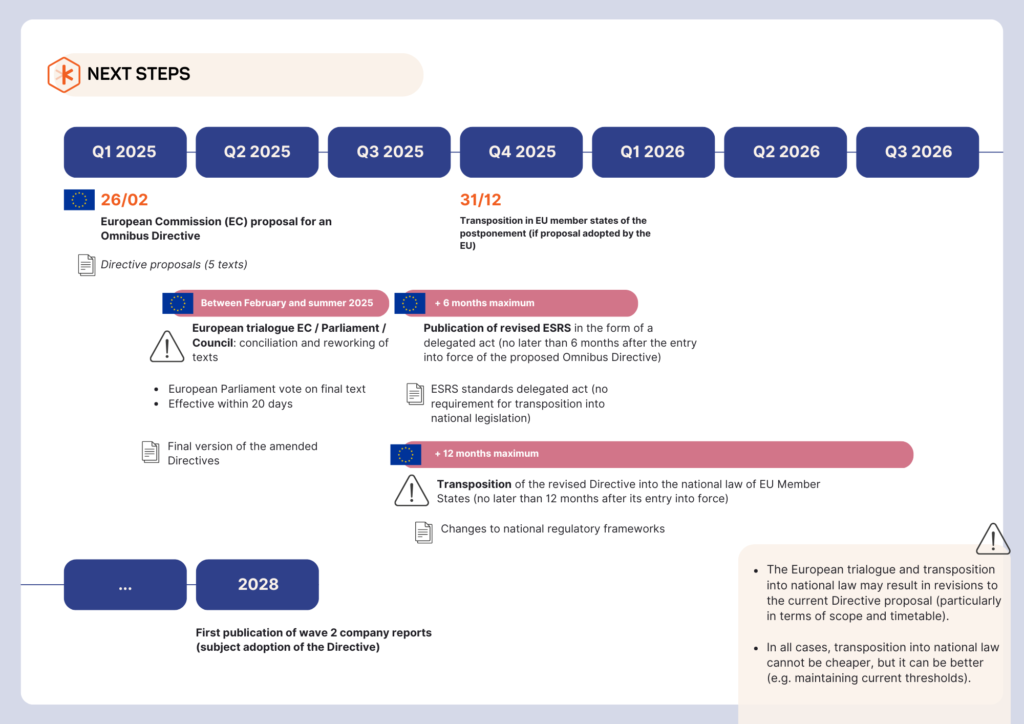

5. Calendar of next steps

The text published on February 26 is only a proposal for a Directive: the legislative process will take many more months, during which the text may be revised!

We propose a timetable of the next steps, assuming that the European trialogue takes place by the summer, given the “urgency” of the situation.

See the content of the proposed Directive :

> Proposal for a Directive of the EU Parliament and the Council amending CSRD and CS3D (2025.02.26)